Introduction to Economics: The Laws of Supply and Demand

Understanding the laws of supply and demand are central to understanding how the capitalist economy operates. Since we rely on market forces instead of government forces to distribute goods and services there must be some method for determining who gets the products that are produced. This is where supply and demand come in. By themselves the laws of supply and demand give us basic information, but when combined together the are

the key to distribution in the market economy… price.

What is demand?

Demand is comprised of three things.

- Desire

- Ability to pay

- Willingness to pay

It is not enough to merely want or desire an item. One must show the ability to pay and then the willingness to pay. If all three conditions are not me then the demand is not real. This, by the way, is the purpose of advertising. While many may want a product it is quite another to be willing to pay. Advertising attempts to move a consumer from mere want to action. These day even

condition two may not stand in the way of a consumer. With the advent of credit cards we are able to purchase products without the current ability to pay. Many stores and car dealers even offer on the spot credit though the interest rate may be quite high.

What factors alter your desire, willingness and ability to pay for products? Some factors include consumer income, consumer tastes the prices of related products like substitutes for that product of items that may complement that product.

Marginal utility – extra satisfaction a consumer gets by purchasing one more unit of a product.

Diminishing Marginal Utility: The more units one buys the less eager one is to buy more. Think of diminishing marginal utility this way. It is a hot summer day and you’re sweating bullets. You come across a lemonade stand and gulp down a glass. It tasted great so you want another. This second glass is marginal utility. But now you reach for a third glass. Suddenly your stomach is bloated and you’re feeling sick. That’s diminishing marginal utility!

There are two types of changes in demand:

Changes in demand – change in the demand for a product that occurs when price drops.

Changes in the Quantity Demanded – change in the amount of a product demanded regardless of price.

The difference is subtle but important. If the demand of ice cream goes up in the summer it is because consumers demand has truly increased, clearly it is hot. In the case the business can most likely raise prices without suffering a drop in sales. This is a change in quantity demanded. If sales of ice cream were to increase in January as a result of a price cut, however, the information we would be receiving is that the demand was artificially

manipulated. It really tells us that actual demand is low and that extra efforts had to be made to increase sales. This is change in demand.

When there is a change in amount purchased (tied to demand) due to lower prices and surplus spending money it is called the income effect. Income effect basically happens when salaries are on the rise.

Another economic phenomenon tied to demand is Substitution Effect. This states that as prices drop consumers will buy more than usual at the expense of a different product. Take a sale at the mall for example. If jeans are on sale for a great price consumers will by extra jeans even if they had previously planned to buy something else. This is that great deal you just cannot pass up. What would the opportunity cost be? That item you passed up and substituted for.

The Law of Demand:

Quantity demanded in inversely proportional to price.

Simply put, the higher the price, the lower the demand and the lower the price, the higher the demand.

In numbers it would look like so:

Cookies

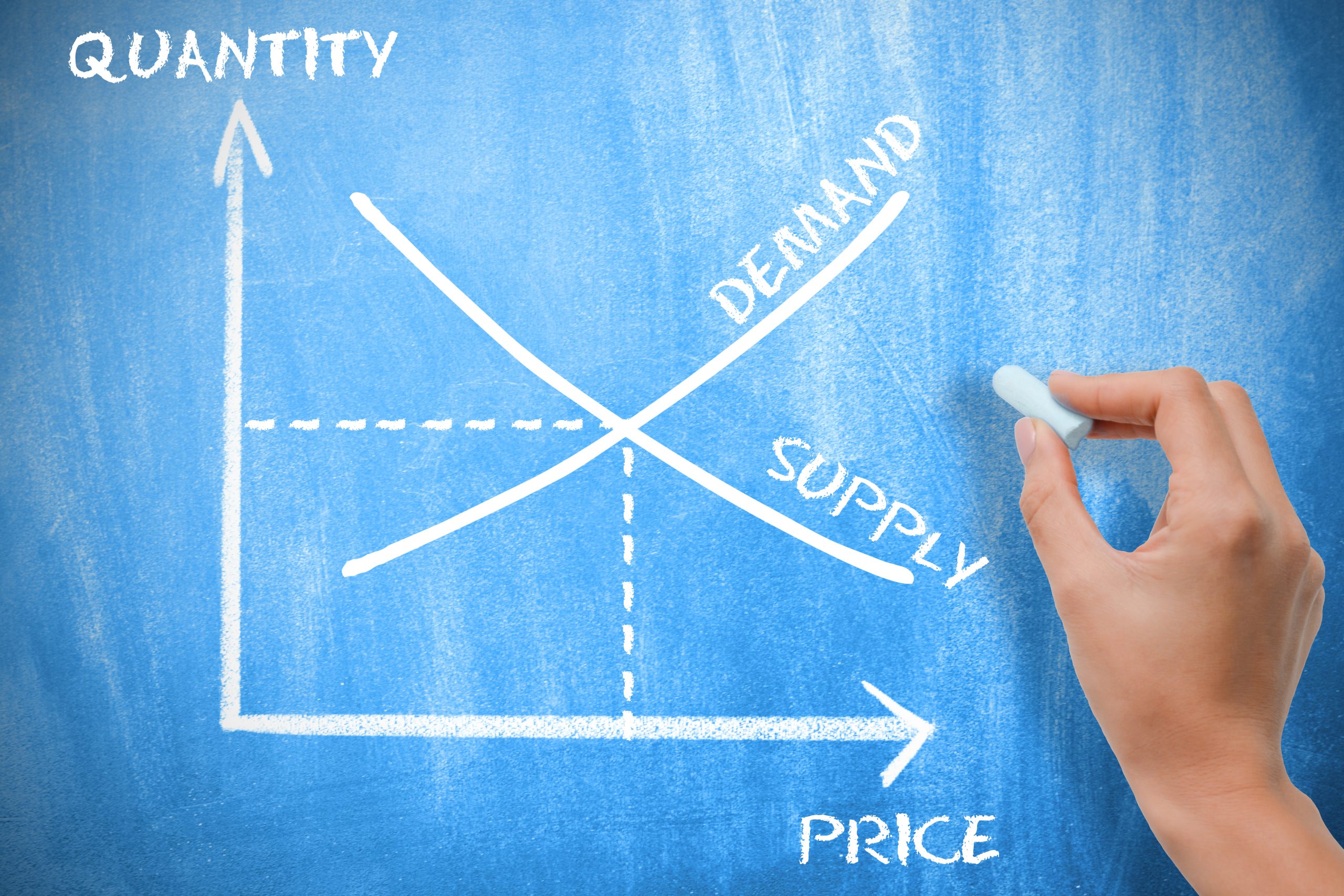

Economists also like to look at things graphically. It enables us to see the quantity and price on a limitless scale. To do this we plot what is known as a demand curve. The price is always on the vertical axis and the quantity is always on the horizontal axis.

The Law of Supply

Quantity supplied is directly proportional to price.

Clearly the law of supply is the opposite of the law of demand. Don’t these both make sense to you? Consumers want to pay as little as they can. They will buy more as the price drops. Sellers, on the other hand, want to be able to charge as much as they can. They will be willing to make more and sell more as the price goes up. This way they can maximize profits.

Numerically a supply schedule would look like this:

Cookies

Market or Equilibrium Price

Now that we have covered both demand and supply we have to combine both together. The place where what sellers are willing to sell for and buyers are willing to buy for is called market or equilibrium price. This is the price the product will sell for. Price is negotiation between the buyers and the sellers.

To figure out price one has to law the supply and demand next top each other.

Chip Cookies

The market price for cookies in this graph is 30 cents. The quantity sold and bought is 1100 cookies.

WHY PRICES ARE IMPORTANT IN A MARKET ECONOMY

Prices are key ingredients in our economy because they make things happen. If buyers want to own some items badly enough, they will pay more for them. When sellers want to sell some items badly enough, they will lower their prices. Prices play such an important role in economic life that the United States is often described as a price-directed market economy. Let us see

why.

1. Act as Signals to Buyers and Sellers. One of the things that prices do is carry information to buyers and sellers. When prices are low enough, they send a “buy” signal to buyers (consumers), who can now afford the things they want. When prices are high enough, they send a “sell” signal to sellers

(retailers), who can now earn a profit at the new price.

2. Encourage Efficient Production. Prices encourage business people to produce their goods at the lowest possible cost. The less it costs to produce an item, the more likely it is that its producers will earn a profit.

Firms that are efficient will produce more goods with fewer raw materials than firms that are inefficient. Producers strive for efficiency as a way of increasing their profits. While these efforts are in the best interests of the sellers, all of us may benefit because we are provided with the things we want at lower costs.

3. Determine Who Will Receive the Things Produced. Finally, prices help to determine who will receive the economy’s output of goods and services. The price that a worker receives for doing a job is called a wage. The amount of this wage determines how much the worker has to spend. What the worker can buy with those wages will depend, in turn, upon the prices of the goods and services the worker would like to own.

Sample Essay - The Laws of Supply and Demand

The laws of supply and demand are two of the most fundamental principles in economics. They describe the relationship between the quantity of a good or service that is supplied and the quantity that is demanded at a given price.

The Law of Supply

The law of supply states that the quantity of a good or service that is supplied increases as the price of that good or service increases. This is because producers are willing to produce and sell more of a good or service when the price is higher, as they can earn more profit.

The law of supply can be illustrated by a supply curve, which is a graph that shows the relationship between the price of a good or service and the quantity supplied. The supply curve typically slopes upward, indicating that the quantity supplied increases as the price increases.

The Law of Demand

The law of demand states that the quantity of a good or service that is demanded decreases as the price of that good or service increases. This is because consumers are less willing to buy a good or service when the price is higher.

The law of demand can be illustrated by a demand curve, which is a graph that shows the relationship between the price of a good or service and the quantity demanded. The demand curve typically slopes downward, indicating that the quantity demanded decreases as the price increases.

Market Equilibrium

The equilibrium price is the price at which the quantity of a good or service supplied is equal to the quantity demanded. This is the price at which the market is in balance.

The equilibrium price is determined by the intersection of the supply and demand curves. At the equilibrium price, there is no surplus or shortage of the good or service.

Examples of the Laws of Supply and Demand

Here are some examples of how the laws of supply and demand work in the real world:

- The price of gasoline: If the price of gasoline goes up, producers will be willing to produce and sell more gasoline, as they can earn more profit. However, consumers will be less willing to buy gasoline, as it will be more expensive. This will lead to a new equilibrium price for gasoline, which will be higher than the old equilibrium price.

- The price of housing: If the price of housing goes up, builders will be willing to build more houses, as they can earn more profit. However, buyers will be less willing to buy houses, as they will be more expensive. This will lead to a new equilibrium price for housing, which will be higher than the old equilibrium price.

- The price of tickets to a concert: If the price of tickets to a concert goes up, the concert promoter will be able to sell more tickets, as they will generate more revenue. However, fewer people will be willing to buy tickets, as they will be more expensive. This will lead to a new equilibrium price for concert tickets, which will be higher than the old equilibrium price.

Applications of the Laws of Supply and Demand

The laws of supply and demand have a wide range of applications in the real world. They can be used to:

- Set prices: Businesses use the laws of supply and demand to set prices for their products and services. They want to set prices at a level that will maximize their profits, which is typically the equilibrium price.

- Make predictions: Economists use the laws of supply and demand to make predictions about the future behavior of markets. For example, they can predict how the price of a good or service will change if there is a change in the supply or demand for that good or service.

- Develop government policies: Governments use the laws of supply and demand to develop policies that affect the economy. For example, they may use taxes or subsidies to increase or decrease the supply or demand for a particular good or service.

Conclusion

The laws of supply and demand are two of the most fundamental principles in economics. They describe the relationship between the quantity of a good or service that is supplied and the quantity that is demanded at a given price. The laws of supply and demand have a wide range of applications in the real world, and they can be used to set prices, make predictions, and develop government policies.

Additional Considerations for Harvard Students

As a Harvard student, you are likely to be interested in more complex and nuanced applications of the laws of supply and demand. Here are a few additional things to consider:

- The impact of non-price factors: The laws of supply and demand typically focus on the impact of price on the quantity supplied and demanded. However, there are also a number of non-price factors that can affect supply and demand. For example, the supply of a good or service may be affected by the cost of inputs, the availability of technology, and government regulations. The demand for a good or service may be affected by consumer preferences, income, and the prices of related goods and services.

The impact of uncertainty: Uncertainty can have a significant impact on the supply and demand of goods and services. For example, if businesses are uncertain about the future economic outlook, they may be less willing to invest in new production facilities. This can lead to a decrease in the supply of goods and services. Similarly, if consumers are uncertain about the future, they may be less willing to spend money. This can lead to a decrease in the demand for goods and services.

The role of market power: Market power is the ability of a firm or group of firms to influence the price of a good or service. Firms with market power may be able to charge higher prices or produce lower quantities than they would if there was more competition in the market. For example, if a firm has a monopoly on the production of a particular good, it will be able to charge a higher price for that good than it would if there were other firms producing the same good.

The impact of technology: Technology can have a significant impact on the supply and demand of goods and services. For example, new technologies can lead to new products and services being developed. New technologies can also lead to the cost of producing and distributing goods and services being reduced. For example, the development of the internet has made it easier and cheaper for businesses to reach consumers around the world. This has led to an increase in the supply of many goods and services, as businesses are now able to sell to a wider range of customers.

Conclusion

The laws of supply and demand are a powerful tool for understanding how markets work. By understanding the laws of supply and demand, you can better understand the forces that influence the prices of goods and services. You can also better understand how government policies and other factors can affect the market.

Additional Thoughts for Students

As a student, you are likely to be interested in more complex and nuanced applications of the laws of supply and demand. Here are a few additional things to consider:

- The impact of globalization: Globalization has made the world economy more interconnected. This has led to an increase in the trade of goods and services between countries. Globalization can also lead to changes in the supply and demand of goods and services in different countries. For example, if a new factory is built in a developing country to produce a particular good, the supply of that good will increase in the global market. This can lead to a decrease in the price of that good in all countries.

- The role of behavioral economics: Behavioral economics is a field of economics that studies the impact of psychological factors on economic decision-making. Behavioral economists have found that people often make decisions that are not in their best economic interests. This can lead to deviations from the predictions of the traditional economic model of supply and demand.

- The role of public policy: Government policies can have a significant impact on the supply and demand of goods and services. For example, governments can use taxes and subsidies to influence the prices of goods and services. Governments can also regulate the production and distribution of goods and services.

The laws of supply and demand are a complex and fascinating topic. There is much more to learn about the laws of supply and demand than can be covered in a short article. However, I hope that this article has given you a good foundation for understanding how the laws of supply and demand work and how they can be applied to a wide range of real-world situations.

Frequently Asked Questions about the Laws of Supply and Demand

The law of supply states that the quantity of a good or service that is supplied increases as the price of that good or service increases. This is because producers are willing to produce and sell more of a good or service when the price is higher, as they can earn more profit.

There are a number of factors that can affect the supply of a good or service. These factors include:

- The cost of inputs: The cost of inputs, such as raw materials and labor, can have a significant impact on the supply of a good or service. If the cost of inputs increases, producers will be less willing to produce and sell that good or service, as they will earn less profit.

- The availability of technology: The availability of technology can also affect the supply of a good or service. If new technologies are developed that make it more efficient to produce a good or service, the supply of that good or service will increase.

- Government regulations: Government regulations can also affect the supply of a good or service. For example, the government may impose safety or environmental regulations that make it more costly to produce a good or service. This can lead to a decrease in the supply of that good or service.

The law of demand states that the quantity of a good or service that is demanded decreases as the price of that good or service increases. This is because consumers are less willing to buy a good or service when the price is higher.

There are a number of factors that can affect the demand for a good or service. These factors include:

- Consumer preferences: Consumer preferences can have a significant impact on the demand for a good or service. If consumers’ preferences change, the demand for a good or service will change accordingly. For example, if there is a new fashion trend for a particular type of clothing, the demand for that type of clothing will increase.

- Income: Income can also affect the demand for a good or service. In general, people with higher incomes are able to buy more goods and services than people with lower incomes. This is because they have more money to spend. However, there are some exceptions to this rule. For example, the demand for some essential goods and services, such as food and housing, is relatively inelastic with respect to income. This means that even if people’s incomes change, their demand for these goods and services does not change very much.

- The prices of related goods and services: The prices of related goods and services can also affect the demand for a good or service. For example, if the price of a substitute good decreases, the demand for the original good will decrease. Similarly, if the price of a complementary good decreases, the demand for the original good will increase.

Market equilibrium is the price at which the quantity of a good or service supplied is equal to the quantity demanded. This is the price at which the market is in balance.

The equilibrium price is determined by the intersection of the supply and demand curves. At the equilibrium price, there is no surplus or shortage of the good or service.

The laws of supply and demand have a wide range of applications in the real world. They can be used to:

- Set prices: Businesses use the laws of supply and demand to set prices for their products and services. They want to set prices at a level that will maximize their profits, which is typically the equilibrium price.

- Make predictions: Economists use the laws of supply and demand to make predictions about the future behavior of markets. For example, they can predict how the price of a good or service will change if there is a change in the supply or demand for that good or service.

- Develop government policies: Governments use the laws of supply and demand to develop policies that affect the economy. For example, they may use taxes or subsidies to increase or decrease the supply or demand for a particular good or service.

Conclusion

The laws of supply and demand are two of the most fundamental principles in economics. They describe the relationship between the quantity of a good or service that is supplied and the quantity that is demanded at a given price. The laws of supply and demand have a wide range of applications in the real world, and they can be used to set prices, make predictions, and develop government policies.

The laws of supply and demand typically focus on the impact of price on the quantity supplied and demanded. However, there are also a number of non-price factors that can affect supply and demand.

- Supply: Non-price factors that can affect supply include:

- The cost of inputs, such as raw materials and labor.

- The availability of technology.

- Government regulations.

- Natural disasters, such as floods and earthquakes.

- Natural resources.

- Weather conditions.

- Demand: Non-price factors that can affect demand include:

- Consumer preferences.

- Income.

- The prices of related goods and services.

- Consumer expectations.

- Population growth.

- Advertising and marketing.

The law of supply and demand states that the price of a good or service will rise if demand exceeds supply, and will fall if supply exceeds demand.

When demand exceeds supply, producers are able to charge higher prices for their goods and services. This is because consumers are willing to pay more for a good or service if there is a shortage of that good or service.

When supply exceeds demand, producers have to lower prices for their goods and services in order to sell them. This is because consumers are less willing to pay for a good or service if there is a surplus of that good or service.

Elasticity is a measure of how responsive the quantity supplied or demanded of a good or service is to a change in price.

- A good or service is said to be elastic if the quantity supplied or demanded changes significantly in response to a change in price.

- A good or service is said to be inelastic if the quantity supplied or demanded does not change very much in response to a change in price.

The elasticity of a good or service depends on a number of factors, including:

- The availability of substitutes and complementary goods.

- The necessity of the good or service.

- The time period considered.

Examples of elastic goods and services include:

- Luxury goods, such as jewelry and yachts.

- Goods that have close substitutes, such as different brands of cereal.

- Goods and services that are not essential for survival, such as entertainment and dining out.

Examples of inelastic goods and services include:

- Essential goods, such as food and housing.

- Goods and services that do not have close substitutes, such as prescription drugs.

- Goods and services that are in high demand, such as gasoline and electricity.

Conclusion

The laws of supply and demand are two of the most fundamental principles in economics. They describe the relationship between the quantity of a good or service that is supplied and the quantity that is demanded at a given price. The laws of supply and demand have a wide range of applications in the real world, and they can be used to understand a variety of economic phenomena.

Additional Thoughts

It is important to note that the laws of supply and demand are just a starting point for understanding how markets work. In the real world, there are a number of other factors that can affect the supply and demand of goods and services, such as government policies, technological change, and globalization.